Pages: 1 2 [3]

|

|

|

Author Author

|

Topic: Fuck Bank of America (Read 24393 times)

|

Merusk

Terracotta Army

Posts: 27449

Badge Whore

|

That's the industry standard answer. My wife has worked for 5/3, US Bank, Citibank and Firstar. They all gave that exact same answer with nearly that exact same wording.

|

The past cannot be changed. The future is yet within your power.

|

|

|

brellium

Terracotta Army

Posts: 1296

|

Overlimit/Overdraft fees are going away anyways with the optout requirements being put in effect later this year. |

"One must see in every human being only that which is worthy of praise. When this is done, one can be a friend to the whole human race. If, however, we look at people from the standpoint of their faults, then being a friend to them is a formidable task."

Abdul-Bahá

|

|

|

slog

Terracotta Army

Posts: 8234

|

Overlimit/Overdraft fees are going away anyways with the optout requirements being put in effect later this year. This isn't one of those fees. |

Friends don't let Friends vote for Boomers

|

|

|

brellium

Terracotta Army

Posts: 1296

|

This isn't one of those fees.

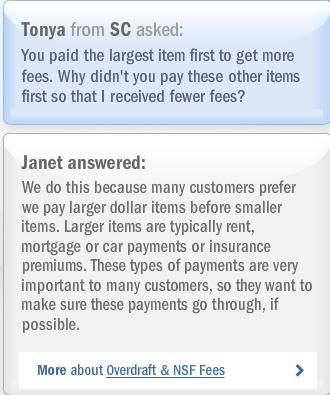

It is one of those fees, the image in question is the "talk off" for the method Bank of America uses for posting withdraws to a checking account. With the new changes to be implemented by the OCC/Fed, requiring an "opt in" for an account to be assessed overdraft fees taking place later this year, banks are responding by either doing away with overdraft charges or the practice of ordering deposit account draws based on the amount of the draw. stupid affect/effect |

|

|

|

« Last Edit: February 28, 2010, 12:18:37 AM by brellium »

|

|

"One must see in every human being only that which is worthy of praise. When this is done, one can be a friend to the whole human race. If, however, we look at people from the standpoint of their faults, then being a friend to them is a formidable task."

Abdul-Bahá

|

|

|

HaemishM

Staff Emeritus

Posts: 42666

the Confederate flag underneath the stone in my class ring

|

They aren't doing away with the fees. They are requiring you to opt in on overdraft "protection." Meaning if you overdraft when using an ATM or a debit card, they won't let the transaction go through unlike now, where they let it go through and charge you a ridiculously large fee on top of it. If you opt-in, it's business as usual, which is why the banks are trying hard to convince folks to opt-in.

|

|

|

|

slog

Terracotta Army

Posts: 8234

|

In other words, If you have 1000 dollars in the bank, and write checks for 900, 200, 200, 200 and 200 dollars, you are getting 4 overdraft fees, just like you did before. BOA explains it better than I do "Opting-Out"

You can ask us not to authorize or pay a transaction unless you have enough available funds in your account at the time to cover the transaction. This is often called "opting-out." Your opt-out request applies to all transactions debit card purchases, atm withdrawals, checks and other withdrawals, transfers and payments. If you opt-out, please note that your account may still become overdrawn and you may incur overdrafts, overdraft item fees and nsf: returned item fees.

Here are some common examples of how opting-out can affect your transactions.

* You want to use your debit card for a purchase or to make an atm withdrawal; however, at the time you initiate the transaction, you do not have enough available funds in your account. In this case, we do not authorize the transaction; we decline it.

* You have written a check for payment; however, at the time we receive the check, you do not have enough available funds in your account. In this case, we return the check unpaid and charge you an nsf: returned item fee.

* You have preauthorized electronic payments from your checking account, such as your insurance premium, mortgage payment or utility payment. However, at the time of a preauthorized payment, you do not have enough available funds in your checking account. In this case, we decline the transaction and charge you an nsf: returned item fee.

For some situations, you may still get overdrafts and overdraft item fees, even though you opted-out. Here are some common examples.

* You use your debit card to pay for gas. If your available balance is $25 and a gas station requests an authorization of $1, the transaction will be authorized. However, if your actual purchase is $45, this will result in a negative $20 balance and we charge you an overdraft item fee.

* You want to use your debit card to purchase a gift. The merchant asks us to authorize the purchase amount, which we do because at that time you have enough available funds in your account to cover the purchase. Before the merchant sends the transaction to us for payment, other payments or withdrawals come through. So, when we receive the transaction for payment, you do not have sufficient funds in your account to cover the debit card purchase. In this case, we pay the debit card purchase and charge you an overdraft item fee.

|

|

|

|

« Last Edit: February 28, 2010, 11:01:17 AM by slog »

|

|

Friends don't let Friends vote for Boomers

|

|

|

Merusk

Terracotta Army

Posts: 27449

Badge Whore

|

The preauthorized withdraws are where folks are really going to get fucked if they opt-out. I can see those NSF:returned item fees doubling or more within the next few months. From talking to people, I get that they forget about automatic withdrawals for their utilities and other stuff all the time, or forget what date they'll be coming out.

|

The past cannot be changed. The future is yet within your power.

|

|

|

brellium

Terracotta Army

Posts: 1296

|

|

"One must see in every human being only that which is worthy of praise. When this is done, one can be a friend to the whole human race. If, however, we look at people from the standpoint of their faults, then being a friend to them is a formidable task."

Abdul-Bahá

|

|

|

slog

Terracotta Army

Posts: 8234

|

You are misunderstanding. That article is only talking about Debit card and Credit card purchases, the jumps to other things without giving the bigger picture. It's also written by a moron. |

|

|

|

« Last Edit: February 28, 2010, 04:55:44 PM by slog »

|

|

Friends don't let Friends vote for Boomers

|

|

|

|

Stormwaltz

Terracotta Army

Posts: 2918

|

|

Nothing in this post represents the views of my current or previous employers.

"Isn't that just like an elf? Brings a spell to a gun fight."

"Sci-Fi writers don't invent the future, they market it."

- Henry Cobb

|

|

|

Lantyssa

Terracotta Army

Posts: 20848

|

"We're really tired of hearing from this woman whose home we incorrectly seized. What a total bitch."

|

Hahahaha! I'm really good at this!

|

|

|

|

Sheepherder

Terracotta Army

Posts: 5192

|

So uhh... criminal charges?

|

|

|

|

|

Oban

Terracotta Army

Posts: 4662

|

|

Palin 2012 : Let's go out with a bang!

|

|

|

schild

Administrator

Posts: 60350

|

More like a singular manager. :\ |

|

|

|

|

Krakrok

Terracotta Army

Posts: 2190

|

Schwab called up a couple weeks ago and informed me that VISA told them my credit card had been compromised and was currently being used in another state.

Once someone gets a credit card number they do a "tasting" of ~$1 to see if it works and then go try to buy a bunch of big stuff. Or so Schwab claims anyway. They claimed the big purchases were denied. I haven't seen anything show up on the statement but they closed the card and sent me a new one.

The interesting thing about the story is that they list a "undisclosed third party" as the source of the credit card number leak. And VISA is the one that informed them? I want to know who the "undisclosed third party" is.

|

|

|

|

|

Furiously

Terracotta Army

Posts: 7199

|

Anyone you have used your credit card with. I've had a waiter at a restaurant steal ours and buy an iphone. (Charge didn't go through).

|

|

|

|

Krakrok

Terracotta Army

Posts: 2190

|

Anyone you have used your credit card with. I've had a waiter at a restaurant steal ours and buy an iphone. (Charge didn't go through).

Right. "undisclosed third party" sounds like a big customer database that was compromised though. Verses something like "unknown third party". |

|

|

|

|

|

Pages: 1 2 [3]

|

|

|

|